Life insurance is an important investment for anyone who wants to protect their loved ones financially in case of an unexpected death. It provides a lump-sum payment to the beneficiary, which can be used to cover expenses like mortgage payments, funeral costs, and other outstanding debts.

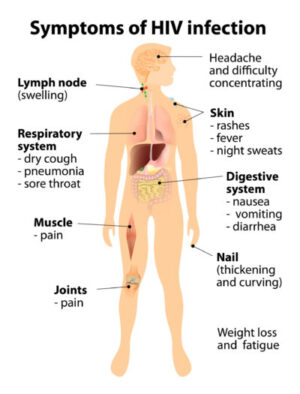

However, for individuals living with HIV or AIDS, the process of obtaining life insurance can be a bit more challenging. Many people with HIV or AIDS assume that they will not qualify for life insurance, or they may have misconceptions about the process.

In this article, we will answer some of the most common questions people with HIV or AIDS usually have about life insurance. Our goal is to provide you with the information you need to make informed decisions and qualify for the best life insurance policy possible.

Frequently Asked Questions

Can I qualify for life insurance if I have HIV or AIDS?

Yes, individuals who have been diagnosed as HIV positive without experiencing symptoms of AIDS may be able to qualify for a traditional life insurance policy. However, the underwriting process for these policies can be more stringent than for individuals without HIV or AIDS. Those with AIDS, on the other hand, will likely only be able to potentially qualify for a guaranteed issue life insurance policy. Guaranteed issue policies do not require medical exams or health screenings and are generally more expensive with lower coverage limits. It’s important to work with an experienced life insurance agent who specializes in coverage for people with HIV or AIDS to find the best policy options available.

Do life insurance companies consider being HIV positive different from having AIDS?

Yes, life insurance companies do consider being HIV positive different from having AIDS. HIV is a virus that can lead to the development of AIDS over time. HIV-positive individuals who are receiving treatment and have a relatively stable immune system may be able to qualify for traditional life insurance policies, whereas those who have progressed to AIDS will likely only be able to qualify for a guaranteed issue life insurance policy. The underwriting process for these policies can be more stringent for individuals with AIDS or advanced HIV due to the increased health risks associated with the condition.

How does my HIV or AIDS status affect my life insurance premiums?

For individuals with HIV only, their life insurance premiums will likely be higher than someone without the virus due to the increased health risks associated with the condition. The severity of the condition and the individual’s overall health will also be factors in determining the premium rate. However, for those applying for a guaranteed issue life insurance policy, the premiums are not based on an individual’s health status and are generally more expensive with lower coverage limits.

Can I get life insurance if I’m currently taking antiretroviral therapy?

Yes, individuals with HIV who are currently taking antiretroviral therapy (ART) may be able to qualify for life insurance. ART is a type of medication that can help to control the HIV virus, prevent disease progression, and improve overall health. Life insurance companies may require documentation of the individual’s current treatment plan and medical history to determine their eligibility for coverage. The severity of the condition and the individual’s overall health will also be factors in determining the premium rate.

What kind of documentation will I need to provide when applying for life insurance with HIV or AIDS?

When applying for life insurance with HIV or AIDS, you will typically need to provide documentation that confirms your diagnosis and current health status. The specific documentation required may vary depending on the insurance company and the type of policy you are applying for, but may include:

- Medical records: You will likely need to provide copies of your medical records that show your HIV or AIDS diagnosis, your current treatment plan, and your overall health status. This may include lab results, doctor’s notes, and other relevant medical documents.

- Medication history: You may also need to provide information about any medications you are currently taking or have taken in the past to manage your HIV or AIDS.

- Lifestyle information: Insurance companies may also ask for information about your lifestyle habits, such as your diet, exercise routine, smoking history, and any other factors that could impact your overall health.

- Other health conditions: You may need to disclose any other health conditions you have in addition to HIV or AIDS, as these may impact your overall risk profile and affect your eligibility for coverage.

How do I find a life insurance company that specializes in coverage for people with HIV or AIDS?

Finding a life insurance company that specializes in coverage for people with HIV or AIDS can be challenging, but there are a few key strategies you can use to help narrow down your options:

- Do your research: Start by doing some research online to find insurance companies that offer coverage for people with HIV or AIDS. Look for companies that have experience working with individuals in your situation, and check their ratings and reviews to ensure they have a strong reputation for customer service and reliability.

- Work with an agent: One of the best ways to find a life insurance company that specializes in coverage for people with HIV or AIDS is to work with an experienced life insurance agent. They can help you understand the policies available, compare rates and coverage options, and identify the best options for your specific needs.

- Ask for referrals: If you know other people living with HIV or AIDS who have obtained life insurance, consider asking them for referrals to insurance companies or agents who they have had a positive experience with.

- Contact advocacy groups: There are a number of advocacy groups and organizations that specialize in providing support and resources for people living with HIV or AIDS. These groups may be able to provide recommendations for insurance companies or agents who can help you find the coverage you need.

Ultimately, the most important factor in finding the right life insurance policy for you will be working with an experienced agent who understands your unique situation and can guide you through the process of finding the right coverage.

Can I apply for life insurance if I have a history of injection drug use?

Yes, you can apply for life insurance if you have a history of injection drug use, but your eligibility for coverage and the cost of your premiums may be affected by this history. Injection drug use is considered a high-risk behavior by life insurance companies, as it can increase your risk of developing certain health conditions or contracting infectious diseases.

When applying for life insurance, you will typically be asked to disclose any history of drug use, including injection drug use. You may also be asked to undergo a medical exam or provide other documentation to help the insurance company assess your overall health status.

Based on this information, the insurance company will determine whether to approve your application and what premium rates to charge. If you have a history of injection drug use, you may be charged higher premiums than someone who does not have this history. However, the specific impact on your premiums will depend on a variety of factors, including your current health status, the type of policy you are applying for, and the insurance company’s underwriting guidelines.

Will I need to undergo a medical exam when applying for life insurance with HIV or AIDS?

If you are applying for a traditional life insurance policy with HIV or AIDS, you will likely need to undergo a medical exam as part of the underwriting process. The exam will typically involve basic health assessments such as measuring your height and weight, taking your blood pressure, and drawing blood to check for any underlying health conditions.

If you are applying for a guaranteed issue life insurance policy, you will not typically be required to undergo a medical exam. These policies are designed to provide coverage to individuals who are unable to obtain traditional life insurance due to pre-existing medical conditions, so they generally do not require a medical exam or health questionnaire.

It’s important to note that while a guaranteed issue policy may be easier to obtain if you have HIV or AIDS, these policies often come with higher premiums and lower coverage limits than traditional life insurance policies. This is because the insurance company is taking on a greater risk by offering coverage without requiring a medical exam or health questionnaire.

Ultimately, the type of life insurance policy you choose will depend on your specific needs and circumstances, as well as the underwriting requirements

What factors do life insurance companies consider when evaluating my application for coverage?

Life insurance companies consider a variety of factors when evaluating an application for coverage. These factors help the insurance company assess the level of risk associated with providing coverage to the applicant, and determine whether to approve the application and at what premium rate. Some of the key factors that life insurance companies consider include:

- Age: Age is an important factor because it can be a predictor of health and life expectancy.

- Gender: Gender can be a factor because women typically have longer life expectancies than men.

- Health history: The applicant’s medical history is an important factor in determining their risk level. This includes any pre-existing medical conditions, family history of illness, and lifestyle habits such as smoking or drinking.

- Medical exams: If required, the results of a medical exam will be evaluated to assess the applicant’s overall health status.

- Medications: If the applicant is taking any prescription medications, the insurance company will want to know what they are and why they are being taken.

- Occupation: Certain occupations may be considered riskier than others, and the insurance company will want to know what the applicant’s occupation is.

- Hobbies: Certain hobbies or activities, such as extreme sports, may increase the risk of injury or death, and can impact the cost of premiums.

- Financial history: The applicant’s financial history, including credit score and income, may be considered in the underwriting process.

- Insurance history: The applicant’s history with other insurance policies, including any claims made, may also be considered.

All of these factors, and potentially others, will be evaluated by the insurance company to determine the level of risk associated with providing coverage to the applicant. Based on this assessment, the company will then decide whether to approve the application, and if so, at what premium rate.

How much life insurance coverage can I qualify for with HIV or AIDS?

If you can qualify for a traditional life insurance policy with HIV or AIDS, the amount of coverage you can qualify for will depend on a variety of factors including your health status, age, and financial situation. However, if you are only able to qualify for a guaranteed issue life insurance policy due to your HIV or AIDS diagnosis, the coverage amount will typically be capped at a relatively low amount, such as $25,000. This is because guaranteed issue policies are designed to provide coverage to individuals who may not be able to obtain traditional life insurance due to pre-existing medical conditions, and as a result, they often come with higher premiums and lower coverage limits.

Can I apply for both term and permanent life insurance with HIV or AIDS?

Yes, you can apply for both term and permanent life insurance with HIV or AIDS, but the availability of each type of policy and the level of coverage you can qualify for may vary depending on your health status and other factors.

Term life insurance provides coverage for a specific period of time, typically 10 to 30 years, and is generally less expensive than permanent life insurance. If you have only tested positive for HIV and are in relatively good health, you may be able to qualify for a term life insurance policy with a standard or substandard rating, depending on the severity of your condition.

Permanent life insurance, on the other hand, provides coverage for the rest of your life and includes an investment component that can build cash value over time. Permanent life insurance policies can be more expensive than term policies, but they offer more long-term security and flexibility.

If you have only tested positive for HIV and are in good health, you may be able to qualify for a permanent life insurance policy with a standard or substandard rating. However, if your condition is more severe or if you have other health issues, you may only be able to qualify for a guaranteed issue policy with a low coverage limit. It’s important to speak with an experienced insurance agent or broker who can help you understand your options and find the right policy for your needs.

Will my life insurance policy pay out if I pass away from HIV or AIDS-related causes?

Yes, if you have a life insurance policy and pass away from HIV or AIDS-related causes, your policy will typically pay out a death benefit to your designated beneficiary or beneficiaries. This is true for both traditional life insurance policies and guaranteed issue policies that are specifically designed for individuals with HIV or AIDS.

It’s important to note that in some cases, there may be a waiting period before the death benefit is paid out, particularly if you are applying for a guaranteed issue policy. Additionally, if your HIV or AIDS diagnosis was not disclosed during the application process, your beneficiaries may not be entitled to receive the death benefit. This is why it’s important to be honest and transparent when applying for life insurance and to work with an experienced insurance agent or broker who can help you find the right policy for your needs.

How can I improve my chances of qualifying for affordable life insurance with HIV or AIDS?

There are several things you can do to improve your chances of qualifying for affordable life insurance with HIV or AIDS:

- Work with an experienced insurance agent or broker who has expertise in helping individuals with HIV or AIDS find the right policy. They can help you navigate the application process, provide guidance on what documentation is needed, and help you find policies that offer the coverage you need at a price you can afford.

- Be honest and transparent about your HIV or AIDS diagnosis during the application process. Lying or withholding information can result in your policy being voided or your beneficiaries being denied the death benefit.

- Maintain good overall health by following your doctor’s orders, taking any prescribed medications, and leading a healthy lifestyle. The better your overall health, the more likely you are to qualify for affordable coverage.

- Consider applying for a traditional life insurance policy before your HIV or AIDS condition becomes more severe. The earlier you apply, the more likely you are to qualify for a policy with more favorable terms and rates.

- Consider applying for a guaranteed issue life insurance policy if you are unable to qualify for a traditional policy due to your HIV or AIDS diagnosis. While these policies may have lower coverage limits and higher premiums, they can still provide important financial protection for you and your loved ones.