Life insurance is a crucial financial tool that provides a safety net for your loved ones in case of your untimely demise. It helps ensure that your family members can maintain their standard of living and meet their financial obligations after you’re gone. However, if you have asthma, you may have concerns about whether you can qualify for life insurance coverage and, if so, what the premiums might be.

To help address these concerns, we’ve put together a list of some of the most common questions people with asthma have about life insurance and provided answers to help you make informed decisions and find the best life insurance policy possible.

Frequently asked questions

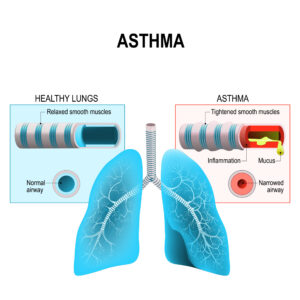

Can I get life insurance if I have asthma?

Yes, you can get life insurance if you have asthma. Having asthma doesn’t automatically disqualify you from getting coverage. However, your asthma may affect your ability to qualify for certain types of policies and may impact your premiums. The severity of your asthma and how well it’s controlled will play a role in determining your eligibility for coverage. In some cases, insurance companies may require additional information or medical exams to assess the risk associated with your asthma.

Will having asthma affect my life insurance premiums?

Yes, having asthma can potentially affect your life insurance premiums. Insurance companies typically consider several factors when determining premiums, including your age, gender, overall health, family medical history, and lifestyle habits. Asthma may be considered a pre-existing condition that could impact your risk profile, which can lead to higher premiums. The severity of your asthma and how well it’s controlled will also play a role in determining your premiums. If your asthma is well-managed with medication and you have a good overall health history, your premiums may not be significantly impacted.

What information will I need to provide to the insurance company about my asthma?

When applying for life insurance with asthma, you will likely be asked to provide some information about your condition. The specific information required may vary depending on the insurance company and the policy you’re applying for, but some common information includes:

- Type of asthma you have (e.g., allergic asthma, exercise-induced asthma)

- Age of onset of asthma

- Frequency and severity of asthma symptoms

- Medications you’re taking to manage your asthma

- Triggers that worsen your asthma symptoms (e.g., pollen, exercise)

- Any hospitalizations or emergency room visits related to your asthma

- Results of any pulmonary function tests or other diagnostic tests related to your asthma

- Any other medical conditions you have that may be related to or impact your asthma.

It’s important to provide accurate and detailed information about your asthma to the insurance company to ensure you receive an accurate quote and that there are no issues with your policy in the event of a claim.

How severe does my asthma have to be for it to affect my life insurance rates?

The severity of your asthma and how well it’s controlled will play a role in determining your life insurance rates. Mild asthma that is well-controlled with medication may have little to no impact on your rates. However, if your asthma is more severe and requires frequent hospitalizations or emergency room visits, or if you have been diagnosed with chronic obstructive pulmonary disease (COPD), your rates may be higher. Insurance companies use actuarial tables and risk assessments to determine rates, so it’s important to disclose all information about your asthma when applying for life insurance. The more severe your asthma is, the higher the risk you may pose to the insurance company, which can result in higher premiums.

Will my asthma medication impact my ability to get life insurance?

In general, taking medication to manage your asthma should not prevent you from getting life insurance coverage. However, the type and dosage of medication you’re taking may impact your rates. Insurance companies will typically consider the medications you’re taking, their dosages, and how frequently you take them when assessing your risk profile. If your asthma is well-controlled with medication, your rates may not be significantly impacted. However, if you’re taking high doses of medication or if your asthma is not well-managed, you may be considered a higher risk and may face higher premiums.

How long do I need to be symptom-free before applying for life insurance with asthma?

There is no set period of time that you need to be symptom-free before applying for life insurance with asthma. However, insurance companies will typically consider your medical history and overall health when assessing your risk profile. If your asthma is well-controlled and you have a good overall health history, your rates may not be significantly impacted. If you’ve had recent exacerbations or hospitalizations related to your asthma, this may impact your rates. It’s important to be honest and accurate about your asthma history when applying for life insurance, as failing to disclose this information could result in a denial of coverage or a claim being denied later on. If you’re unsure about whether you’re ready to apply for life insurance, it’s best to speak with a licensed insurance agent who can help you assess your options and find the best policy for your needs.

Will the insurance company require a medical exam for life insurance with asthma?

Whether or not an insurance company will require a medical exam when applying for life insurance with asthma will depend on several factors, such as the type of policy, the insurance company’s underwriting guidelines, and the severity of your asthma.

For many standard term life insurance policies, a medical exam is typically required. This exam will usually include a review of your medical history, a physical exam, and blood and urine tests. If your asthma is well-controlled and you have a good overall health history, the medical exam may not impact your rates significantly. However, if your asthma is more severe, a medical exam may result in higher rates.

Some insurance companies offer no medical exam life insurance policies, which may be a good option if you have well-controlled asthma but want to avoid a medical exam. However, these policies typically have higher premiums and lower coverage amounts compared to traditional policies that require a medical exam.

What type of life insurance policy is best for someone with asthma?

The type of life insurance policy that is best for someone with asthma will depend on your individual needs and situation. Here are a few options to consider:

- Term Life Insurance: Term life insurance provides coverage for a set period of time, typically 10, 20, or 30 years. This type of policy is often more affordable than permanent life insurance and may be a good option if you need coverage for a specific period of time, such as to pay off a mortgage or provide for your children until they reach adulthood.

- Whole Life Insurance: Whole life insurance provides lifelong coverage and includes a cash value component that grows over time. This type of policy is often more expensive than term life insurance but may be a good option if you need lifelong coverage and want to build cash value over time.

- Guaranteed Issue Life Insurance: Guaranteed issue life insurance is a type of no medical exam life insurance policy that does not require any medical underwriting. This type of policy may be a good option if you have a pre-existing condition such as asthma and are unable to qualify for traditional life insurance policies.

Can I get life insurance if I smoke and have asthma?

It may be possible to obtain life insurance coverage even if you smoke and have asthma, but it’s unlikely that you’ll be able to qualify for a traditional life insurance policy. Smoking is a significant risk factor for many health conditions, including asthma, and insurance companies will view you as a high-risk applicant.

However, some insurance companies offer guaranteed issue life insurance policies, which do not require any medical underwriting or health questions. These policies are typically more expensive than traditional life insurance policies and may have lower coverage amounts, but they may be a good option if you have pre-existing conditions that make it difficult to qualify for traditional coverage.

Can my life insurance policy be cancelled if I develop complications related to my asthma?

No, your life insurance policy cannot be cancelled if you develop complications related to your asthma once the policy is in force. Once a life insurance policy is issued, it is a binding contract between you and the insurance company, and as long as you continue to pay your premiums on time, the policy cannot be cancelled due to any changes in your health status.

However, it’s important to note that if you were not honest about your asthma history or other health conditions when you applied for the policy, the insurance company may have grounds to contest a claim or cancel the policy during the contestability period, which is typically the first two years after the policy is issued.

What if I have a family history of asthma? Will it affect my life insurance rates?

If you have a family history of asthma, it may not necessarily affect your life insurance rates directly, but it’s important to disclose this information when applying for life insurance. Insurance companies may ask about your family medical history on the application, and this information could be used to help determine your overall risk level.

If you have a family history of asthma, it’s possible that the insurance company may view you as a higher risk applicant, particularly if you have a personal history of asthma as well. However, each insurance company has its own underwriting guidelines and rating factors, so the impact of a family history of asthma on your life insurance rates may vary.

Can I still get life insurance if I participate in activities that trigger my asthma, such as sports or exercise?

Yes, you can still get life insurance if you participate in activities that trigger your asthma, such as sports or exercise. However, your participation in these activities may be considered by the insurance company when determining your risk level and setting your premiums.

Insurance companies may ask about your participation in sports or exercise on the application, and may also ask for additional information about the severity and frequency of your asthma symptoms. Depending on the information provided, the insurance company may adjust your rates to reflect the increased risk associated with your activities.

Will my life insurance policy payout be affected if my death is related to my asthma?

If your life insurance policy is in force and you pass away as a result of asthma, your beneficiaries should be entitled to receive the death benefit specified in the policy. As long as you were truthful in your application and disclosed your asthma history, the insurance company should honor the policy and pay out the death benefit to your beneficiaries.

It’s important to note, however, that some life insurance policies may have exclusions or limitations for certain medical conditions, including asthma. These exclusions may limit or exclude coverage for death related to asthma or related complications. It’s important to review your policy carefully and speak with a licensed insurance agent if you have any questions or concerns.

Additionally, if you pass away within the first two years of the policy being in force, the insurance company may investigate the cause of death more closely to ensure that there was no fraud or misrepresentation on the application. If it is determined that you were not truthful about your asthma history or other health conditions, the insurance company may have grounds to contest the claim or deny the death benefit.